When The Amount Of Medical School Debt Seems Hopeless

Graduating from residency or fellowship with large amount of student debt can feel a lot like standing in front of a mountain. It’s hard to see the end when the debt load is overwhelming. Most of the people I know who have over a quarter million in debt fall into one of two categories. The first group is individuals who feel that the amount of medical school debt seems hopeless. These individuals are usually afraid to get started on debt repayment. The second, and much smaller group, are those doctors who are laser focused on conquering their debt.

The Psychology Of Debt Payoff

It doesn’t matter if it’s debt payoff, weight loss, or hiking up a mountain. Every goal needs milestones along the way and a plan. A good example of setting realistic goals for a big problem is weight loss. Asking a patient to lose 100-200 pounds will most likely seem hopeless to the patient. If I walked in the room and told the patient they need to lose that amount much weight, they most likely will stop listening because to them it seems to impossible.

Losing weight or paying off a large amount of debt might be the end goal, but it should not be the primary focus in these individuals. You don’t climb a mountain looking at the summit the entire time. Stick to the path, work hard, and take breaks to see your progression.

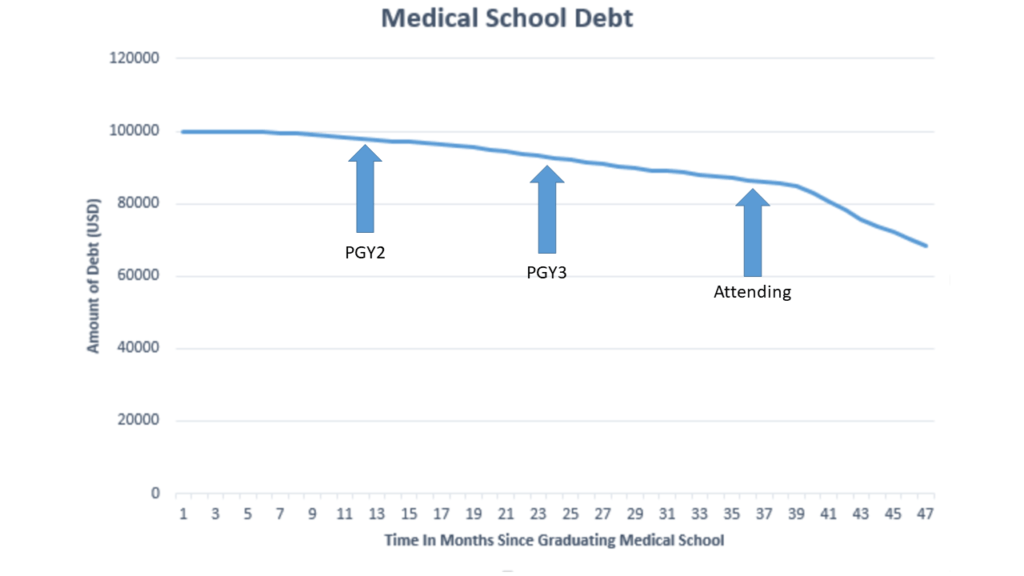

Instead of focusing on the end goal the entire time, focus on quicker more obtainable goals. If I ask my patients to cut out one soda a day, I’m likely to get better results. Instead of being discouraged that my patient “only” lost 5 pounds in a month out of the 200 pound goal, I congratulate them on that first step. The same rule goes to doctors who start their debt repayment journey. It seemed hopeless when I started off paying $600 a month, but as you can see from my post several months ago, my dept repayment over time has made a lot of progress.

The Snowball Vs Avalanche Medical School Debt Repayment Methods

The snowball method was made popular by Dave Ramsey. It also got a recent boost in popularity due to a study that seemed to confirm that this method often does a better job of getting people motivated to get out of debt.

The snowball method is described in three steps:

- Pay the minimum payment on all of your loans

- Any leftover money for debt repayment is then applied to the loan with the smallest balance

- Once that debt is paid off, then devote all left over money to the next loan with the smallest balance till all loans are paid off

The snowball method does not take into account interest rates on any of the loans. While this may not be financially the most ideal way to save money by paying off debt, it gets people paying down their debt.

The Avalanche Method

The Avalanche method to pay off debts focuses primarily on interest rates. Mathematically this method gives the borrower (you) the least amount of interest paid on the loans. The steps are the same as above for the snowball method with one exception. Instead of paying the debt with the smallest balance, you pay the debt with the highest interest rate first and work your way down.

While this is the best way to financially take care of debt, this method can seem hopeless to some since progress seems slow.

An Example Using Dr. Average.

Let’s take the average medical doctor who graduates from residency and decides to buy a new place as a new attending. Let’s also assume that Dr. Average makes $200,000 a year. Here is what Dr. Average debt might look like upon graduation.

- Student loans $200,000 @ 6.8%

- Car loan 15,000 @ 3%

- Furniture loan (you’ve gotta live on something in your new place) $2,000 @ 4%

- House / Condo $300,000 @ 3.6%

Does Snowball vs Avalanche Matter?

As you can tell Dr. Average has quite a bit of debt, but still less than 3 times their gross income. If Dr. Average lives in Texas, his or her gross paycheck will be ~$11,000 per month. Let’s say that 34% of Dr. Average paycheck goes to debt repayment. How long till they are debt free?

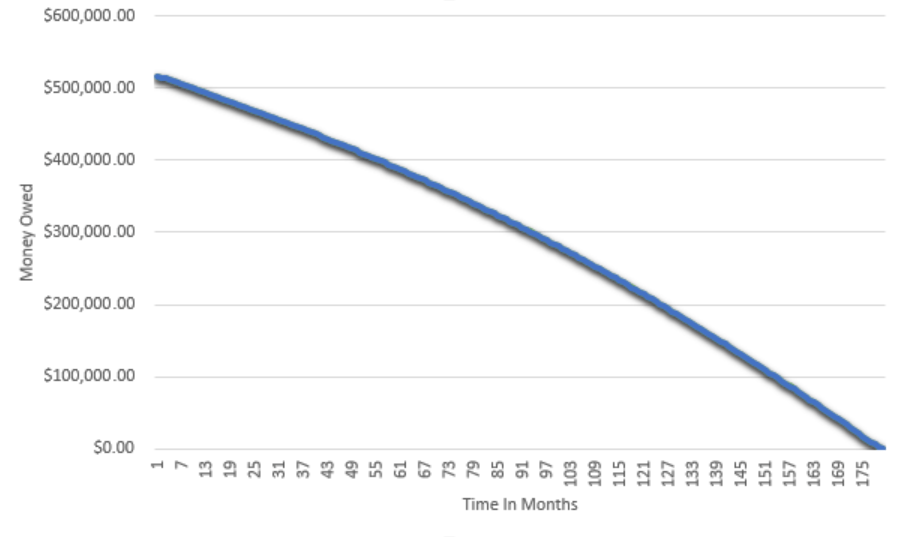

Turns out that in this example snowball vs avalanche method makes little difference due to Dr. Average income level and relatively similar t.

Yes there are two lines there. One is black and the other is blue.

The avalanche comes out ahead by one month and a little over $2,000 in interest saved. You can play with the numbers and see how your loans would vary if you did avalanche vs snowball method. Here is a good calculator to compare the two.

There are two main reasons why the avalanche vs snowball method does not have a huge impact on the average doctor’s debt.

- Doctors have a large income potential which can minimize the percent of money spend on necessities (electricity, food, gas)

- Most doctors have debts with medium levels of interest rates. (4-7%).

Debts with high interest rates such as credit cards or payday loans are situations when the avalanche method saves more money compared to the snowball method. Since most doctors debt lies in a mortgage or student loan, the benefit of using one method over the other matters very little. What does matter, is motivation to pay down the debt.

Getting Motivated To Pay Off Debt

Staying motivated and getting started are the two largest psychological factors for paying down large amounts of student debt. There is no better time than now to start paying down debt. Whatever method motivates you, keep at it. In the example above, the difference over 178 months was only about $2000 or $12 a month.

My fiance and I have more spreadsheets than I would like to admit. Each month I add to the spreadsheets and see a visual progression of my debt. This is my method to stay motivated. I’ve refinanced my loans to save me more than $10,000 over the life of a loan. In effect, I’ve made the avalanche vs snowball method for me a non issues since refinancing saved me even more money. If you’r interest rates are similar to the example above, then it might be in your best interest to refinance also to accelerate debt payoff.

If you have a lot of student loans, it might benefit you to consider refinancing your loans.

Great post. I personally used the snowball method. When I graduated from fellowship I had a lot of various loans (wedding, home, my school loans, wife school loans, 2 car loans, and a mattress loan). I started with the smallest amount debt and moved up from there. It was great to see each debt disappear and gave me the psychologic boost to continue.

I’m glad you mentioned the mattress loan. I got a good laugh because I forgot that my intern year I also took out a loan for my mattress. I figured I needed good sleep and I’m glad I splurged on it. Seeing debt disappear is such a good feeling, but watching compounding interest on my investments grow is 100x better!

Do you have any advice/does this plan change at all for someone with an especially large debt burden? I’m thinking of those with $400k+ due to attending an out-of-state school or a DO school. Is it imperative to choose a high paying specialty?

I wouldn’t say that you HAVE to choose a specialty based on your student loans. However, be aware that choosing a lower pay specialty, such as pediatrics, this will drastically effect your ability to pay off debt compared to that of an orthopedic surgeon. For doctors who have 400k in student loans in a lower paying specialty, I think those doctors will have to ask themselves if they want to have sacrifices and pay down debt quickly or choose a PSLF program. Picking up extra shifts, or doing locum tenens work is a great way to help pay down debt if you’re willing to live like a resident for a little bit longer.

My advise to doctors with that much debt is figure out if you want to hope for student loan forgiveness via a government program or be dedicated to pay off the debt as quickly as possible. Having almost half a million dollars in debt is a big problem, but luckily doctors make a big income that can help pay it down quickly if you stay focused.

Mattress loan? You can get a mattress loan? That reminds me of a couple I helped with their finances once. They had 22 separate loans including a $2K pet loan. Yup, they bought a dog on credit. Despite making $7K a month they couldn’t make ends meet because all their money was servicing debt. Perfect candidates for some Dave Ramsey style intervention.